Aircraft Engine Fuel Systems Market Scope and Size Valuation Expected at 77.05 Billion by 2034

The global aviation industry relies heavily on intricate technological architectures to ensure the safety, efficiency, and unwavering reliability of commercial, military, and general aviation aircraft. At the very heart of this operational framework lies the aircraft engine fuel system. Responsible for storing, managing, regulating, and delivering fuel to the engine at precise pressures and flow rates, these systems are fundamentally critical to flight performance. As the aerospace sector rebounds from past global disruptions and scales up to meet unprecedented modern travel demand, the aircraft engine fuel systems sector is experiencing strategic and steady growth. This evolution is shaped by an intersection of rising passenger traffic, stringent environmental regulations, and the relentless pursuit of fuel efficiency by airline operators worldwide.

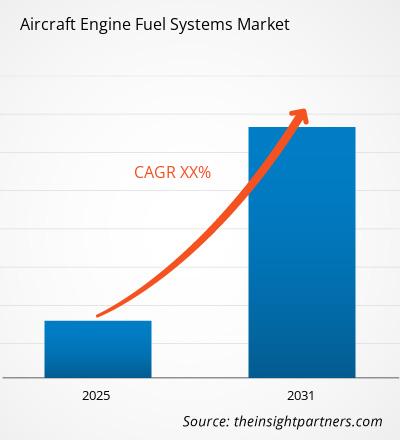

Market Size and Growth Trajectory

The Aircraft Engine Fuel Systems Market size is expected to reach US$ 77.05 Million by 2034 from US$ 51.42 Million in 2025. The market is estimated to record a CAGR of 4.60% from 2026 to 2034.

While the absolute dollar value of this specific component market may appear niche when compared to broader aerospace valuations, it represents a highly specialized, highly regulated, and vital segment of aerospace engineering. This steady compound annual growth rate is largely driven by the natural replacement cycle of aging aircraft fleets, the aggressive procurement of next-generation commercial jetliners, and increased defense spending across major global economies. Commercial airlines operate on notoriously thin profit margins, and aviation fuel historically represents one of their largest continuous operating expenses. Consequently, airlines are heavily invested in acquiring advanced fuel systems that ensure optimal combustion, prevent fuel starvation, and minimize systemic waste.

Key Market Drivers and Dynamics

Several interconnected factors are fueling the steady expansion of this market. First, the surging demand for commercial air travel in emerging economies particularly across the Asia-Pacific and Middle Eastern regions has necessitated substantial fleet expansions. Aircraft manufacturers are working diligently to ramp up production rates to deliver on immense backlogs of both narrow-body and wide-body aircraft. Every single new jet engine off the assembly line requires a sophisticated, fully integrated fuel delivery and management system.

Second, the global military aerospace sector is currently undergoing a profound modernization phase. Advanced fifth-generation fighter jets, heavy transport aircraft, and complex unmanned aerial vehicles (UAVs) require highly robust, fault-tolerant fuel delivery systems capable of functioning seamlessly under extreme G-forces, high altitudes, and drastically fluctuating temperatures.

Furthermore, international regulatory bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) are implementing ever-stricter environmental and noise protocols. This regulatory pressure forces original equipment manufacturers (OEMs) to design systems that maximize fuel economy and reduce overall carbon footprints, thereby accelerating the market demand for sophisticated upgrades and retrofits to existing aircraft.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00015296

Technological Advancements Reshaping the Industry

Innovation remains the cornerstone of the aircraft engine fuel systems sector. Modern fuel systems are far removed from their purely mechanical predecessors of the mid-20th century. Today, they are deeply integrated with Full Authority Digital Engine Control (FADEC) computing systems. These electronic brains constantly monitor flight conditions, throttle positions, air density, and atmospheric variables to meter the exact micro-amount of fuel required, second by second.

Additionally, there is a prominent industry-wide shift toward "lightweighting." Manufacturers are increasingly utilizing advanced composite materials and additive manufacturing (3D printing) to produce complex fuel system components like pumps, intricate valves, and precision metering units. Lighter parts reduce the overall dry weight of the aircraft, which inherently means the aircraft burns less fuel to stay aloft. Furthermore, the rising integration of smart sensors within the fuel lines allows for predictive maintenance. This technology enables ground crews to monitor system health in real-time and identify wearing fuel system components before they fail in transit, significantly reducing costly aircraft downtime.

Key Players in the Market

The competitive landscape of the Aircraft Engine Fuel Systems Market is characterized by intense research and development initiatives, rigorous safety testing, and long-term supply contracts with major aircraft manufacturers like Boeing, Airbus, Lockheed Martin, and Embraer. The industry is highly consolidated, with a select group of legacy aerospace engineering giants dominating the space due to the high barrier to entry and strict certification requirements.

The prominent key players operating in this dynamic market include:

-

Honeywell International Inc.

-

Parker Hannifin Corporation

-

Woodward, Inc.

-

Eaton

-

Triumph Group

-

Collins Aerospace, a Raytheon Technologies company

-

Andair LTD

-

Secondo Mona S.p.A.

-

Crane Aerospace and Electronics

-

Meggitt PLC

Future Outlook

Looking ahead to 2034 and beyond, the Aircraft Engine Fuel Systems Market is poised for transformative technological shifts, primarily dictated by the global aerospace industry’s ambitious commitment to achieving net-zero carbon emissions by 2050. A major focal point for manufacturers will be the widespread adoption of Sustainable Aviation Fuels (SAF) and, eventually, liquid hydrogen propulsion. Future fuel systems will need to be fundamentally re-engineered to handle the unique chemical properties, lower lubricity, and complex thermal dynamics of these alternative power sources. Moreover, as the industry begins actively testing hybrid-electric aircraft architectures, traditional fuel management systems will evolve to bridge the gap between conventional combustion and auxiliary electric power generation. Ultimately, the companies that can successfully adapt their fuel system technologies to align with a greener, smarter, and highly digital aviation ecosystem will be the ones that dominate the skies of tomorrow.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876