Clamshell Packaging Market to Reach USD 18.9 Billion by 2036 | Supported by Growth in Consumer Goods Packaging

According to Future Market Insights (FMI) The global clamshell packaging market is entering a transitional phase where product protection, retail visibility, and sustainability pressures are reshaping how manufacturers, retailers, and logistics providers approach packaging design. Once viewed primarily as a low-cost retail display solution, clamshell packaging is increasingly being repositioned as a strategic packaging format capable of balancing tamper resistance, product presentation, shelf-life extension, and transportation durability across modern retail and e-commerce ecosystems.

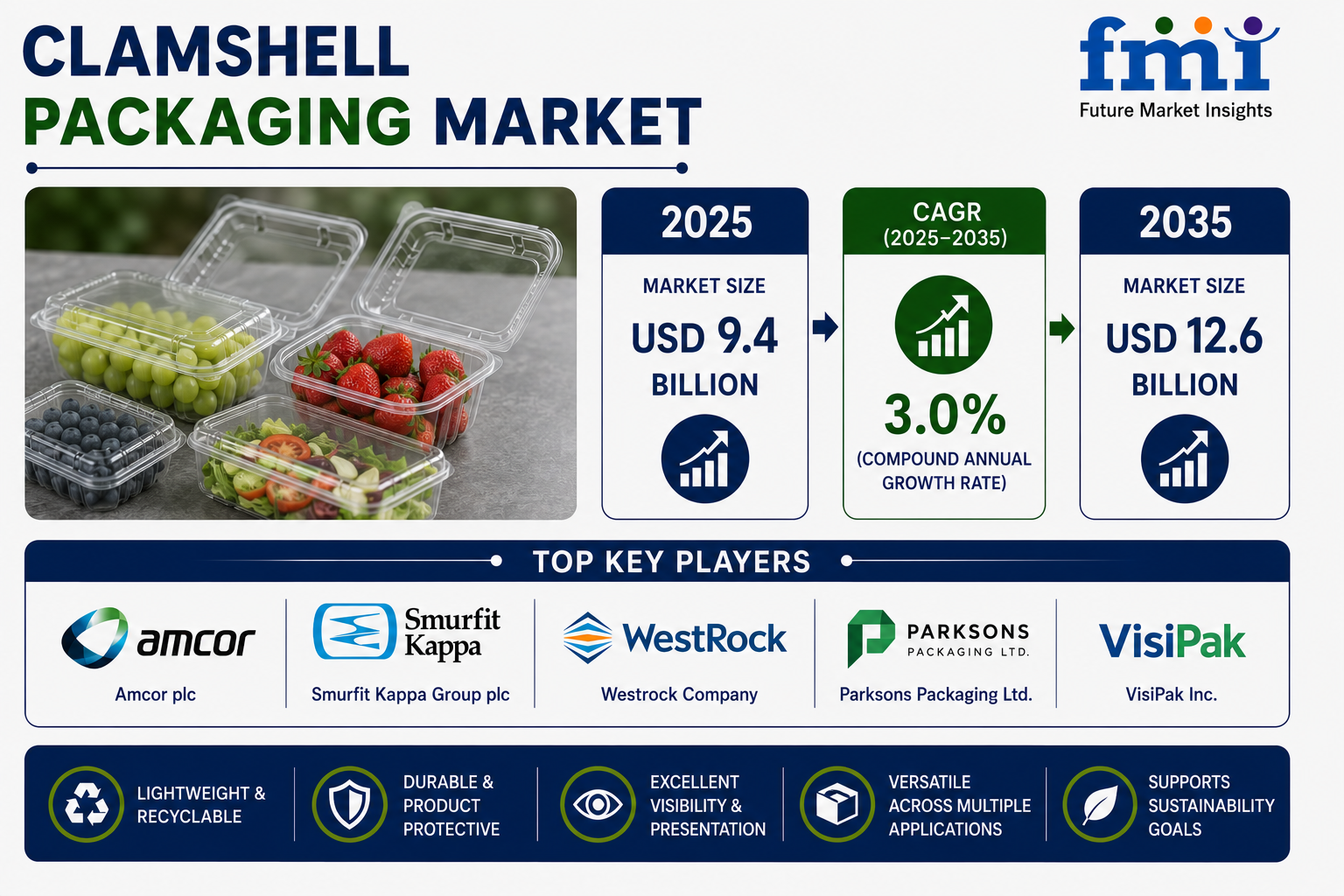

The global clamshell packaging market is projected to grow from USD 9.4 billion in 2025 to USD 12.6 billion by 2035, registering a CAGR of 3.0%. Growth is being supported by rising demand across food packaging, consumer electronics, pharmaceuticals, cosmetics, and organized retail channels where secure, transparent, and visually appealing packaging continues to hold commercial value.

Quick Stats: Clamshell Packaging Market

- Market Size (2025): USD 9.4 billion

- Projected Market Value (2035): USD 12.6 billion

- Forecast CAGR (2025–2035): 3.0%

- Leading Packaging Type: Trays (36.8%)

- Leading Material Type: Plastic (52.4%)

- Top Product Format: 2-Piece Clamshells (41.7%)

- Largest End Use Segment: Food (62.8%)

- Key Growth Regions: North America, Asia-Pacific, Europe

Get Detailed Market Forecasts, Competitive Benchmarking, and Pricing Trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-3573

Clamshell Packaging Is Evolving from Simple Protection to Retail Strategy

The market’s current trajectory reflects a broader shift in packaging priorities across consumer industries. Retailers and brand owners are no longer selecting packaging solely for containment or transport protection. Instead, packaging increasingly functions as:

- A branding surface

- A product visibility tool

- A tamper-evidence mechanism

- A convenience format

- A logistics optimization asset

Clamshell packaging sits at the intersection of these demands because it combines:

- Product transparency

- Structural rigidity

- Shelf-ready presentation

- Stackability

- Consumer convenience

This combination continues to make the format attractive across both physical retail shelves and digital commerce fulfillment systems.

Market Forecast: Moderate Growth Supported by Functional Demand

The market’s 3.0% CAGR reflects a relatively mature packaging category, but one that continues to maintain relevance because of its adaptability across industries.

Growth is being driven by:

- Expansion of organized retail

- Growth in ready-to-eat food consumption

- Rising food delivery volumes

- E-commerce packaging requirements

- Demand for tamper-evident formats

- Consumer preference for visible packaging

At the same time, manufacturers are investing heavily in:

- Recyclable polymers

- Paper-based clamshell alternatives

- Compostable materials

- Lightweight thermoformed structures

These investments are increasingly necessary as regulatory scrutiny around single-use plastics intensifies globally.

Food Industry Remains the Dominant Demand Engine

Food Accounts for 62.8% of Market Share

The food industry continues to anchor the clamshell packaging market because the format aligns closely with modern food retail requirements.

Clamshells are widely used across:

- Fresh produce

- Bakery products

- Ready-to-eat meals

- Frozen foods

- Convenience snacks

Food brands increasingly rely on clamshells because they provide:

- Product visibility

- Freshness protection

- Portion control

- Stackability

- Tamper resistance

The rise of on-the-go consumption patterns and meal delivery ecosystems is further reinforcing demand for durable and presentation-focused packaging formats.

Trays Lead Packaging-Type Demand

Trays Hold 36.8% Share

Tray-based clamshells have emerged as the dominant packaging type because they support:

- Efficient retail stacking

- Easy transportation

- Product compartmentalization

- Enhanced shelf presentation

Their versatility across food and electronics applications gives them broad commercial relevance.

Manufacturers are also introducing:

- Resealable trays

- Multi-compartment designs

- Lightweight structures

- Eco-friendly tray materials

This evolution is helping trays maintain leadership despite growing pressure from flexible packaging alternatives.

Plastic Remains Dominant But Sustainability Pressures Are Intensifying

Plastic Holds 52.4% Share

Plastic remains the leading material because it offers:

- Superior clarity

- Low production cost

- Impact resistance

- Thermoforming flexibility

- Lightweight performance

Materials such as PET, PVC, PP, and PS continue dominating large-scale production lines due to compatibility with high-volume manufacturing systems.

However, sustainability concerns are rapidly changing procurement priorities.

Packaging producers are increasingly investing in:

- Post-consumer recycled plastics

- Bio-based polymers

- Compostable alternatives

- Circular-economy manufacturing systems

This transition is becoming especially important in regions with aggressive packaging waste regulations.

Why 2-Piece Clamshells Continue Leading

2-Piece Formats Hold 41.7% Share

2-piece clamshells remain the preferred product format because they combine:

- Strong sealing performance

- Easy customization

- Tamper evidence

- Consumer convenience

These formats are particularly valuable in:

- Foodservice packaging

- Electronics retail

- Cosmetics packaging

- Pharmaceutical applications

Manufacturers are increasingly improving:

- Opening mechanisms

- Recyclability

- Lightweighting

- Consumer usability

The format’s balance between protection and presentation continues supporting broad commercial adoption.

E-Commerce Is Quietly Reshaping Clamshell Packaging Design

One of the most important structural shifts influencing the market is the rise of e-commerce fulfillment.

Online retail requires packaging that can:

- Withstand transportation stress

- Prevent product tampering

- Reduce damage claims

- Preserve presentation quality

This is especially relevant for:

- Electronics

- Consumer goods

- Meal kits

- Fresh food delivery

As fulfillment networks become more automated, packaging formats that offer:

- Dimensional consistency

- Stacking stability

- Lightweight protection

are becoming increasingly valuable.

Flexible Packaging Remains the Market’s Biggest Competitive Threat

Despite steady growth, clamshell packaging faces rising competition from flexible packaging systems.

Flexible alternatives often provide:

- Lower material consumption

- Reduced transportation costs

- Improved storage efficiency

- Greater sustainability perception

This creates pressure on clamshell producers to justify higher material intensity through:

- Better product protection

- Enhanced retail merchandising

- Improved recyclability

- Premium branding value

The long-term competitiveness of clamshell packaging may increasingly depend on how effectively producers integrate sustainable materials into rigid packaging systems.

Speak to Analyst: Customize insights for your Business Strategy: https://www.futuremarketinsights.com/customization-available/rep-gb-3573

Regional Analysis: Asia-Pacific Emerges as the Strongest Growth Engine

India Leads Regional Growth (6.1% CAGR)

India is projected to be the fastest-growing market due to:

- Rapid expansion of organized retail

- Rising food delivery penetration

- Growth in e-commerce packaging demand

- Increasing convenience-food consumption

Government support for sustainable packaging and retail modernization is also supporting industry expansion.

China Maintains Manufacturing Influence (4.7% CAGR)

China remains a critical production hub because of:

- Packaging material scale

- Thermoforming infrastructure

- Electronics manufacturing concentration

- Export-oriented supply chains

Chinese manufacturers continue influencing pricing and material availability across global packaging markets.

North America Focuses on Convenience and Retail Durability

The United States market remains highly influenced by:

- E-commerce growth

- Convenience consumption

- Retail-ready packaging demand

- Food safety expectations

Consumer preference for secure and tamper-evident packaging continues supporting adoption across grocery and retail categories.

Europe Pushes Sustainability Innovation

Markets such as Germany, France, and United Kingdom are increasingly shaping innovation around:

- Compostable packaging

- Paper-based clamshells

- Circular packaging systems

- Reduced plastic dependency

Regulatory pressure is accelerating material transformation across the European packaging sector.

Competitive Landscape: Sustainability and Material Innovation Become Core Differentiators

The competitive environment is becoming increasingly shaped by:

- Material innovation

- Recycling compatibility

- Retail partnerships

- Automation compatibility

- Global manufacturing reach

Key Companies Include:

- Amcor plc

- Smurfit Kappa Group plc

- WestRock Company

- Sonoco Products Company

- Placon Corporation

- Novolex Company

Recent industry developments highlight the market’s sustainability transition:

- Huhtamaki launched paper-based clamshell packaging for fresh fruit

- NatureWorks partnered with PAC Packaging on bio-based produce packaging

- The Sustainable Packaging Coalition introduced new recycling guidance for clamshell materials

Strategic Implications for Industry Stakeholders

For Food Producers

- Tamper-evident and presentation-ready formats remain commercially valuable

- Sustainable tray innovation may become a competitive differentiator

For Retailers

- Product visibility continues influencing purchase behavior

- Packaging durability reduces transportation losses and shrinkage

For Packaging Manufacturers

- Material innovation is now critical for long-term relevance

- Paper-based and recyclable clamshell systems represent future growth areas

For Investors

- Mature growth profiles favor companies with:

- Sustainable material capabilities

- Thermoforming innovation

- Circular packaging integration

- Retail and e-commerce exposure

Future Outlook: The Industry Moves Toward Sustainable Rigid Packaging

The clamshell packaging market is unlikely to disappear despite growing sustainability criticism. Instead, the category is evolving toward: